Blog

Complete Guide to KWSP Housing Withdrawal Malaysia | RumahHQ

Did you know that over 70 percent of Malaysian employees tap into their KWSP savings to support home ownership? The KWSP housing withdrawal programme opens doors for many by allowing use of retirement funds for buying, building, or renovating residential properties. This financial tool could make your dream home more attainable while preserving your long-term savings. Understanding key rules and benefits helps you maximize this opportunity and avoid common mistakes that might delay your plans.

Key Takeaways

| Point | Details |

|---|---|

| Flexible Housing Withdrawal | Members can leverage KWSP savings for property investments while maintaining long-term financial security, as it allows continuous earning of dividends. |

| Withdrawal Options | The programme includes various types such as Buy House, Housing Loan Instalment, and Build House withdrawals, each catering to specific residential needs. |

| Eligibility Criteria | Applicants must be below 55 years old, meet minimum savings requirements, and comply with specific property types to qualify for withdrawals. |

| Application Process | Comprehensive documentation is essential, including valid identification, financial proof, and completed forms to ensure successful applications. |

Table of Contents

KWSP Housing Withdrawal Explained and Key Concepts

The Employees Provident Fund (KWSP) housing withdrawal programme offers Malaysian workers a strategic pathway to leverage their retirement savings for residential property investments. Understanding this programme can significantly impact your home ownership journey.

According to KWSP’s official guidelines, the Flexible Housing Withdrawal option provides members with unique financial advantages:

- Allows ring-fencing of current and future savings

- Boosts housing loan eligibility

- Maintains savings locked until age 55

- Continues earning dividends during the locked period

- Banks recognize these savings as income for loan qualification

The withdrawal mechanism is designed to support members in achieving their residential property goals without compromising long-term financial security. Members can strategically use a portion of their EPF savings to support home purchases, renovations, or construction projects.

Learn more about maximizing your KWSP savings for home projects, ensuring you make informed decisions about your property investment strategy.

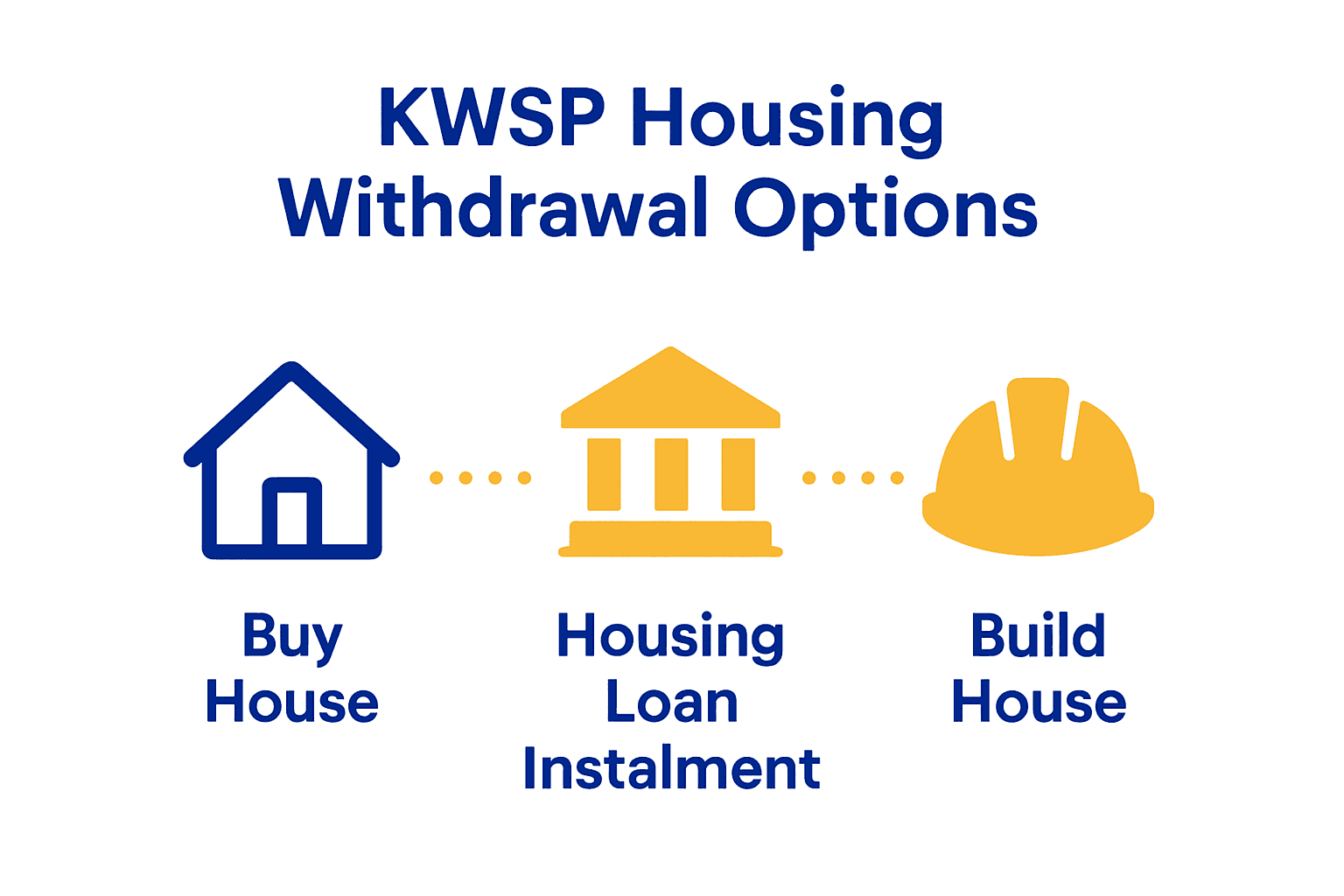

Types of KWSP Withdrawals for Housing Purposes

The Employees Provident Fund (KWSP) offers Malaysian workers multiple strategic housing withdrawal options designed to support different residential property needs. Understanding these withdrawal types can help you make informed financial decisions about your property investments.

Buy House Withdrawal

According to KWSP’s official guidelines, the Buy House Withdrawal provides members with flexible property acquisition opportunities:

- Applicable for purchasing various residential properties

- Covers property types including bungalows, apartments, and SOHO units

- Allows withdrawal for two properties maximum

- Requires sale or disposal of previous property before second withdrawal

- Supports first-time and subsequent home purchases

Housing Loan Instalment Withdrawal

The Housing Loan Instalment Withdrawal offers another strategic financial mechanism. Based on KWSP regulations, this option enables members to:

- Cover monthly loan instalments

- Require minimum six months of consistent loan payments

- Place withdrawn funds into a special dedicated account

- Have distinct eligibility criteria separate from other withdrawal types

Explore how KWSP can help you achieve your home renovation dreams, providing additional insights into maximizing your housing financial strategies.

Eligibility Requirements and Approved Properties

KWSP housing withdrawals come with specific eligibility criteria designed to support Malaysian homeowners and property investors. Understanding these requirements is crucial for successfully accessing your retirement funds for housing purposes.

General Eligibility Criteria

According to KWSP’s official guidelines, the fundamental eligibility requirements include:

- Age limit: Must be below 55 years old

- Minimum savings: At least RM500 in Akaun Sejahtera

- Financing status: Either have an approved housing loan or be self-financing

- Citizenship: Open to Malaysian and non-Malaysian members

Approved Property Types

The housing withdrawal programme supports various residential property types:

- Landed properties (houses)

- Apartments

- Condominiums

- Serviced Apartments

- SOHO (Small Office Home Office) units (requires manual application)

Special Considerations for House Building

Based on KWSP’s build house withdrawal regulations, additional requirements for construction include:

- Land ownership by applicant or spouse

- Construction agreement dated within three years

- Verification of previous property disposal (if applicable)

- Approved loan or self-financing confirmation

Learn more about maximizing your KWSP savings for home projects, ensuring you understand all potential pathways to your dream home.

Application Procedures and Required Documentation

Navigating the KWSP housing withdrawal process requires careful preparation and comprehensive documentation. Understanding the precise requirements can streamline your application and increase your chances of successful approval.

Documentation Checklist for Property Purchase

According to KWSP’s official guidelines, applicants must compile the following essential documents:

- Completed Form KWSP 9C (AHL)

- Comprehensive application checklist

- Valid identification documents

- Recent bank statements

- Sales & Purchase Agreement

- Proof of financing or relationship (if joint application)

- Property disposal evidence (if applicable)

House Building Withdrawal Documentation

Here’s a comparison of the main KWSP housing withdrawal types:

| Withdrawal Type | Key Purpose | Eligibility Highlights | Major Required Documents |

|---|---|---|---|

| Buy House Withdrawal | Property purchase | Under age 55 Min RM500 savings |

Form 9C Sales & Purchase Bank statements |

| Housing Loan Instalment | Cover monthly loan repayments | 6+ months loan payments Active loan |

Form 9C Loan statements Recent bank statements |

| Build House Withdrawal | Residential construction on owned land | Land ownership Construction agreement |

Form 9C Land titles Construction agreement |

Based on KWSP’s build house withdrawal regulations, additional documentation for construction projects includes:

- Form 9C submission

- Financing proof (loan approval letter, contractor receipts)

- Land ownership documentation

- Land purchase agreement

- Title deed

- Official land search certificate

- Detailed construction agreement

- Local authority approvals

- Joint application relationship verification

Application Submission Process

To ensure a smooth application:

- Verify all documents are current and correctly completed

- Arrange documents in the recommended order

- Make copies of all submitted materials

- Consider professional guidance if uncertain about requirements

Explore our comprehensive guide on maximizing KWSP savings for home projects, which provides additional insights into navigating the withdrawal process effectively.

Legal Protections, Risks, and Common Pitfalls

Navigating KWSP housing withdrawals requires a comprehensive understanding of potential legal risks and protective measures. Being well-informed can help you avoid costly mistakes and ensure a smooth financial transaction.

Critical Legal Documentation

According to legal experts, the Carian Rasmi (official land search) plays a crucial role in protecting your property investment:

- Verifies legal property ownership

- Identifies potential property encumbrances

- Confirms property details and legal status

- Prevents fraudulent property transactions

- Essential for KWSP withdrawal application approval

Common Withdrawal Application Risks

Potential pitfalls in the KWSP housing withdrawal process include:

- Incomplete documentation

- Outdated identification documents

- Incorrect form submissions

- Missing financial proof

- Failure to update personal information

Risk Mitigation Strategies

To protect your financial interests:

- Maintain updated personal documentation

- Conduct thorough property due diligence

- Verify all information before submission

- Seek professional legal advice when uncertain

- Keep comprehensive records of all transactions

Important: An outdated or incomplete Carian Rasmi can result in immediate application rejection.

Explore our comprehensive guide on maximizing KWSP savings for home projects, providing additional insights into navigating potential legal complexities.

Financial Implications and Comparison with Alternatives

Choosing the right housing withdrawal strategy requires careful financial analysis and understanding of potential long-term implications. The KWSP offers unique mechanisms that can significantly impact your property investment and retirement planning.

Flexible Housing Withdrawal Strategy

According to KWSP’s official guidelines, the Flexible Housing Withdrawal presents several strategic financial advantages:

- Enhances loan eligibility

- Factors future EPF contributions as income

- Potential for qualifying for larger loans

- Continues earning dividends during locked period

Comparative Financial Considerations

Key financial trade-offs to evaluate:

-

Loan Qualification

- KWSP withdrawal can improve borrowing capacity

- Provides alternative to traditional income verification

-

Savings Restrictions

- Funds remain locked until age 55

- Limited pre-retirement access

- Potential opportunity cost of fund immobilization

Alternative Financing Options

Compared to traditional financing methods, KWSP housing withdrawal offers:

- Lower interest exposure

- Reduced external borrowing dependency

- Utilization of existing retirement savings

- Potential tax efficiency

Caution: Carefully assess long-term retirement impact before making withdrawals.

Learn more about maximizing your KWSP savings for home projects, ensuring comprehensive financial strategy planning.

Make Your KWSP Housing Withdrawal Work for You – Build with Confidence

Struggling to make the most of your KWSP housing withdrawal because of confusing procedures, documentation hurdles or doubts about project budgeting? If you feel overwhelmed by the strict requirements and want to ensure every ringgit is well invested in your dream home or renovation, you are not alone. Our expertise at RumahHQ directly addresses the pain points featured in this guide – from navigating flexible housing withdrawals and documentation to planning worry-free construction that truly maximises your hard-earned retirement savings.

Do not let uncertainty stall your plans. Discover how RumahHQ transforms the way you approach residential upgrades by offering a full suite of end-to-end services, including transparent project pricing, free design consultations and structure warranties for peace of mind. We are devoted to helping you streamline every step, whether you are preparing documentation, seeking government approvals or searching for honest builders. Visit our homepage today to request your free consultation or talk to our team about flexible financing options using your KWSP withdrawal. Make each RM count and secure real quality with your next project – act now while rates and incentives remain available.

Frequently Asked Questions

What is the KWSP housing withdrawal program?

The KWSP housing withdrawal program allows Malaysian workers to leverage their Employees Provident Fund (KWSP) savings to purchase, renovate, or construct residential properties while maintaining long-term financial security.

What are the different types of withdrawals available for housing purposes under KWSP?

The KWSP offers multiple withdrawal options: Buy House Withdrawal for property purchases, Housing Loan Instalment Withdrawal to cover monthly loan repayments, and Build House Withdrawal for constructing homes on owned land.

What are the eligibility requirements to withdraw from KWSP for housing purposes?

To be eligible, members must be under 55 years old, have a minimum of RM500 in their Akaun Sejahtera, possess an approved housing loan or self-financing, and are open to both Malaysian and non-Malaysian members.

What documentation is required for a KWSP housing withdrawal application?

Essential documents include a completed Form KWSP 9C, identification papers, recent bank statements, a Sales & Purchase Agreement, and any necessary proof of financing or property disposal. Additional documents may be required for construction withdrawals.

Recommended

Source link

kontraktor rumah

bina rumah

pinjaman lppsa

pengeluaran kwsp

spesifikasi rumah

rumah batu-bata

pelan rumah

rekabentuk rumah

bina rumah atas tanah sendiri

kontraktor rumah selangor

rumah banglo